In this week’s episode of Mondays with Matthew, Windermere Chief Economist Matthew Gardner kicks off a series of episodes in which he answers questions from his followers. The first deals with how COVID-19 will impact buyer behaviors, especially in more urban markets.

Beautifully REMODELED home at 1529 Barnwood Court in Windsor on 1/4 ACRE LOT with GORGEOUS VIEWS of LAKE and OPEN SPACE. Remodels display HIGH QUALITY FINISHES throughout. MASTER SUITE features EXTRAVAGANT SHOWER and walk-in closet. Beautifully HAND-CRAFTED STONE WALL and barnwood beams frame NEW FIREPLACE in the family room. CUSTOM TRIM. Beautiful and private landscaping. Dirt trail behind house leads to fishable ponds and wildlife area. Comes with vegetable garden! Contact Elizabeth Dolton at (970) 396-7233 for your private showing for more information or click the link below for more details.

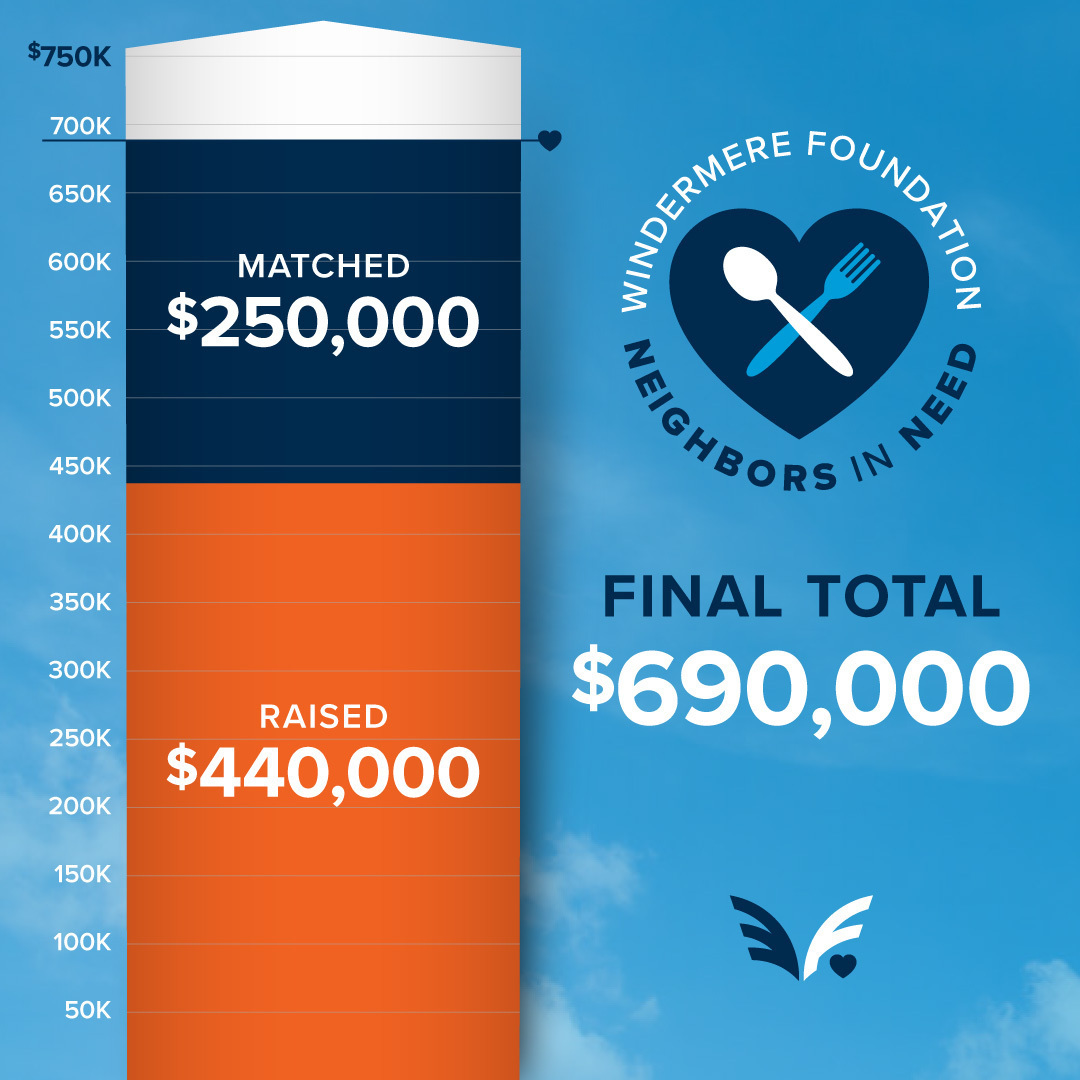

The COVID-19 pandemic has affected populations across the globe, but those who struggle with poverty and count on food programs to meet their basic day-to-day needs are in an especially uncertain place. While coping with increased demand and a bottlenecked pipeline of food supply, food banks are desperate for funds to continue to serve their communities. Because of this, Windermere decided to challenge its offices to raise $250,000, every dollar of which would be matched by the Windermere Foundation and donated to food banks in the areas where Windermere operates. We titled it the “Neighbors in Need” fundraising campaign.

Neighbors in Need kicked off on April 21, with the goal of raising $250,000 by May 5. As word continued to spread, online donations and contributions from both our agents and the public began to increase. Neighbors in Need was given a boost by Seattle Seahawks starting safety Quandre Diggs in a heartfelt message encouraging support. Over the final 24 hours, leading up to the May 5 deadline, support poured in from across the Windermere family as the final figure exceeded the initial goal of $500,000, landing at a total of $690,000.

Neighbors in Need exemplifies Windermere’s deep commitment to supporting our local communities, which traces back to 1989 when the Windermere Foundation first started. Since then, we’ve proudly raised more than $41 million for low-income and homeless families throughout the Western U.S.

On behalf of the Windermere Foundation to all those who joined the effort: Thank you. We could not have made this large of an impact without your help. We are humbled to be able to do our part to help those who need it most during these uncertain times.

We notice a very interesting dynamic in the market right now.

There was clearly a pent-up real estate demand created during the recent time when in-person showings were not allowed. The numbers back it up.

First, a little background. During a portion of “Shelter in Place,” all in-person viewing of properties ceased. Instead, buyers spent time online viewing virtual tours and 3-D photography.

Even though clients could view homes virtually, purchase activity did slow down.

Today, showings are allowed again as long as clear protocols are followed. We’ve implemented a Safe Showings program to keep our clients protected.

Now, to the numbers.

Through the first two weeks of May 2020, the number of closed properties is down compared to the same time period in 2019.

In most cases these closed properties are a result of purchase agreements that were written in April- a time when in-person showings were restricted.

So, a decrease in closings was expected.

However, the number of new written contracts so far this month is up considerably compared to the same time frame last year.

Specifically,

Metro Denver closed properties down 47%

Metro Denver new contracts up 6%

Northern Colorado closed properties down 41%

Northern Colorado new contracts up 19%

So, buyer activity is up compared to last year, even in our current environment.

This speaks to the resiliency of our market and the effect of low interest rates.

Staying organized while uprooting your life and moving from one home to another can feel impossible. Not only are you trying to get the best financial return on your investment, but you might also be working on a tight deadline. There’s also the pressure to keep your home clean and organized at all times for prospective buyers. However, one thing you can be sure of when selling your home is that there will be strangers entering your space, so it’s important for you and your agent to take certain safety precautions. Like so many things in life, they can feel more manageable once written down, so we made this handy checklist.

Go through your medicine cabinets and remove all prescription medications.

Remove or lock up precious belongings and personal information. You will want to store your jewelry, family heirlooms, and personal/financial information in a secure location to keep them from getting misplaced or stolen.

Remove family photos. We recommend removing your family photos during the staging process so potential buyers can see themselves living in the home. It’s also a good way to protect your privacy.

Check your windows and doors for secure closings before and after showings. If someone is looking to get back into your home following a showing or an open house, they will look for weak locks or they might unlock a window or door.

Consider extra security measures such as an alarm system or other monitoring tools like cameras.

Don’t show your own home! If someone you don’t know walks up to your home asking for a showing, don’t let them in. You want to have an agent present to show your home at all times. Agents should have screening precautions to keep you and them safe from potential danger.

Talk to your agent about the following safety precautions:

Do a walk-through with your agent to make sure you have identified everything that needs to be removed or secured, such as medications, belongings, and photos.

Go over your agent’s screening process:

Phone screening prior to showing the home

Process for identifying and qualifying buyers for showings

Their personal safety during showings and open houses

Lockboxes to secure your keys for showings should be up to date. Electronic lockboxes actually track who has had access to your home.

Work with your agent on an open house checklist:

Do they collect contact information of everyone entering the home?

Do they work with a partner to ensure their personal safety?

Go through your home’s entrances and exits and share important household information so your agent can advise how to secure your property while it’s on the market.

Job growth is critical to the health of the housing market, so on this week’s episode of “Mondays with Matthew,” Windermere Chief Economist Matthew Gardner analyzes the effect of COVID-19 on employment and what we can expect for the duration of the year.

April represents the first time we can look at the impact of COVID-19 on a full month of real estate activity.

To no one’s surprise, activity in April in terms of closings and new contracts did slow significantly.

Much of this slowing was caused by in person showings not being allowed for most of the month.

(showings are now allowed again by following Safe Showings protocols)

Here’s what the numbers say…

Closed transactions were down compared to April 2019

26% in Northern Colorado (Larimer & Weld)

27% in Metro Denver

New written purchase agreements were down compared to April 2020

48% in Northern Colorado

44% in Metro Denver

So, while activity did slow, there was nothing resembling a “screeching halt” that took place.

While the way property is shown has certainly changed, the market is still very active and we expect activity to increase even more with showings now being allowed again.

This week our Chief Economist took a deep dive into the numbers to examine the current health crisis versus the housing crisis of 2008.

The reason why? People wonder if we are going to have another housing meltdown nationally and going to see foreclosures and short sales dramatically increase.

It turns out that the numbers show that today’s housing environment is quite different than 2007, right before the housing bubble burst.

Specifically, homeowners are in a vastly different situation with their mortgage compared to the pre-Great Recession’s housing meltdown.

In addition to much higher credit scores and much higher amounts of equity compared to 2007, the most significant difference today is in the amount of ARM mortgages.

Back in years leading up to the housing bubble, Adjustable Rate Mortgages were very prevalent. In 2007 there were just under 13 million active adjustable rate loans, today there are just over 3 million.

The number of those ARMs that would reset within three years was 5 million in 2007 compared to only 320,000 today.

It’s those Adjustable Rate loans resetting to a higher monthly payment that caused such a big part of the housing crisis back in 2008 to 2010.

Back then not only was people’s employment impacted, but many were facing increased monthly mortgage payments.

That’s why there were so many foreclosures and short sales in 2008 to 2010.

That is not the case today and one of many reasons why we don’t foresee a housing meltdown.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link